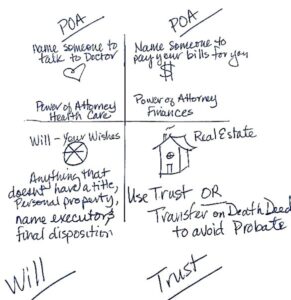

Estate planning includes four components; (1) a Will, (2) Power of Attorney for Finances, (3) Power of Attorney for Health Care, and (4) a Revocable Trust. These are the four parts of anyone’s estate plan. The authority of Powers of Attorney die with you. Everyone needs a Will because everyone has “Stuff”. If you don’t own a house, you don’t need a trust. It’s just that simple.

First, pick a Medical Agent. say you were in a coma, and you had to pick someone to talk to the Doctors for you, and tell them what kind of treatment you would want? Who would you trust to stand up to doctors in order to fulfill what you want? That’s your Agent for your Power of Attorney for Health Care.

NOTE: This power will only be used (1) when the signer is unable to communicate about their own wishes; and (2) if there is a dispute over what treatments should be done, or not done. Otherwise, the Power of Attorney for health care is only used to determine who has the right to sign the body out of the hospital to transmit it to a funeral home or morgue.

Second, Financial issues. Who would you trust to handle your money? Who would you trust to go through your accounts, total up your assets and pay off your debts? Who do you think is responsible enough to handle taking care of your financial assets if you can’t? Who is trustworthy? That’s your agent for your Power of Attorney for Finances.

NOTE: Be careful who you choose for your financial agent. These Powers of Attorney can be easily abused, they can clear out your bank account completely without repercussion. With the advent of online banking, it is usually something long term like dementia that creates a real reason to sign a Financial Power of Attorney form.

Third, Your Will. Who would you want to be in charge of handling your final wishes? Who do you trust to follow your directions? Your Will is a list of final directions, and it’s as simple as: I choose this person to give out what I own, to this list of beneficiaries. You list your personal property, including jewelry, cars, clothing, etc. You can request that everything be sold and the proceeds divided equally between your beneficiaries. Just list what you own, and where you want it to go.

Asset List: Goes to:

Checking account my children

Vehicle charity

Retirement Account to spouse

Consider who you would want to receive sentimental or family heirlooms and put it all down in writing to avoid fights later.

Finally, A Trust holds title to real estate so that it essentially has a “name tag” on it. It avoids probate because the Trust is an agreement between the owners on what should happen to the real estate when one or both Trustees die.

NOTE: A Trust does not avoid creditors, and a Trust only avoids Probate. It does not avoid taxes at all. It merely creates a non-legal private way for real estate to pass to a deceased person’s beneficiaries without going through probate court. Multiple regulations govern Trust administration post-death.

Ready to start your estate planning?

Estate Planning Intake Form

Estate Planning intake form